New Opportunities through Partial Use of the IRBA under CRR III

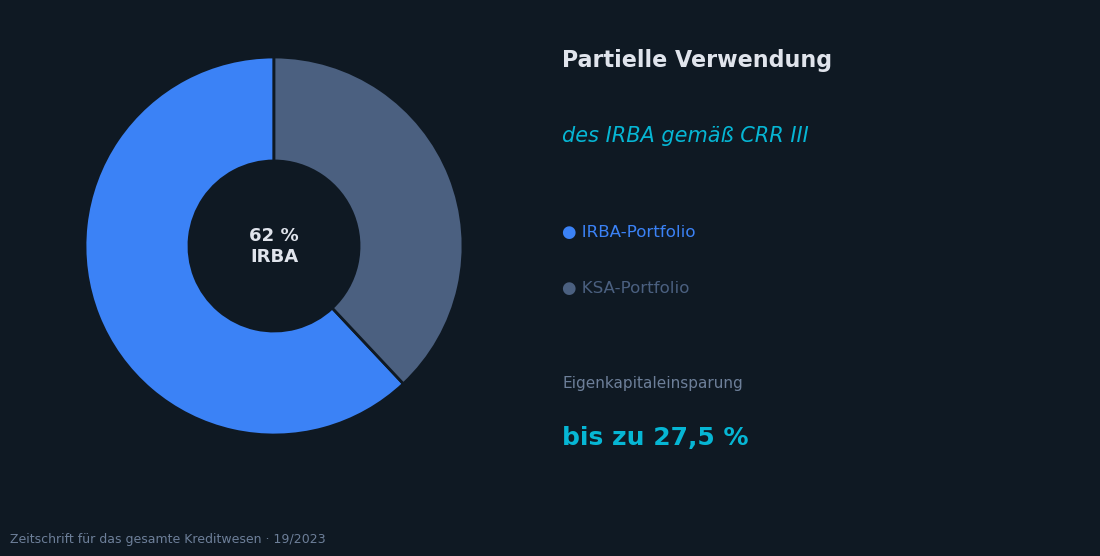

CRR III allows banks for the first time to apply the IRBA selectively to individual credit classes – with potential capital savings of up to 27.5%.

Authors: Manfred Puckhaber, Stephan Vorgrimler, Prof. Dr. Dirk Schieborn

Journal: Zeitschrift für das gesamte Kreditwesen

Reference: Kreditwesen 19/2023

Year of publication: 2023

Abstract

With CRR III, significant changes to capital requirements for credit risk will come into force from 2025. For institutions currently using the Standardised Approach (SA), maintaining the status quo could lead to an increase in capital requirements – driven by higher risk weights and the newly introduced Output Floor.

At the same time, CRR III opens up a new possibility: banks may now permanently apply the IRBA to only a portion of their portfolio, without having to meet the previous minimum coverage ratio of 92%. This partial use allows institutions to selectively migrate those portfolio segments to the IRBA where the effort is justified by the resulting capital relief.

Using the example of a mid-sized cooperative bank, the authors demonstrate how a structured feasibility analysis can be constructed and what savings potential is realistically achievable – in the modelled case study, up to 27.5%.

Practical Relevance

The article provides institutions with a concrete decision-making framework that enables them to strategically leverage the regulatory changes under CRR III – regardless of whether they are already using the IRBA or are only considering entering it.